There’s an age-old saying that the first million is the hardest.

While it’s always harder to start from nothing than to build on something, there’s more to this than first meets the eye.

For the record, we’re not talking about a million dollar paycheck, but rather having a million dollars in investments.

So, let’s find out why is it exactly that the first million dollars gives us the most trouble, and how come the subsequent millions seem to come a lot easier.

How Compounding Interest Works

The first and most important thing on why the first million is the hardest is the nature of compounding interest.

It takes a long time to make a big difference.

Let’s take a look at how compounding works by using this nifty compound interest calculator from Moneyzine.com:

Okay, so here’s an imaginary scenario where you‘d make a one-time investment of $10,000 with a 10% annual interest rate.

As we can see from the graph, there’s really not much going on during the first 10 to 15 years. At 10 year-mark, you’d have a total of $25,937. By the year 25, you’d have $108,347.

If this would continue linearly, it would take a long, long time to achieve $1 million. Such a large amount of money may seem like it’s in the distant future if you’ve just started investing.

Luckily, compound interest works exponentially, not linearly. What it means is that the growth accelerates more the longer you let your interest compound.

Let’s look at our example again.

It took the first 25 years to achieve $98,000 in return. In comparison, about 20 years later between the years 48 and 49, that same $98,000 took only one year to achieve.

So, the first million dollars being the hardest is actually a mathematical fact. It DOES get easier the longer you do it.

The Problem with Starting Early (Or Late)

Building wealth and achieving a millionaire status (and financial independence) takes time.

If you wish to have a million dollars before you retire, you need to start investing as early as possible.

The problem is that when we’re young, we don’t usually have a high income and can barely invest at all. Often we start with negative net worth because of student loans and such, which means we’re already starting from behind.

After we’ve landed a job with a decent salary, we can start to invest more. Of course, by that time people usually start families that require a lot of money.

So, the sweet spot for investing is the time when you’re in your late twenties without children, or in your late forties when your children start to take care of themselves.

What makes the first situation problematic is that if you want to start a family, it doesn’t last long.

The problem with the latter is that if you start to invest in your late forties, it’s somewhat unlikely that you’ll make it to the one million net worth milestone without a high income.

The first million is the hardest because you need to work for the money before it starts to work for you.

The Challenges of Starting Small

Have you ever wondered why the rich seem to always get richer?

Well, it’s obviously mostly due to compounding and passive income, but there’s more to it.

Same Returns, Different Scales

The number one thing money can do is give you opportunities. When you have more capital, you have loads of opportunities to make more money.

Let’s imagine you had an extremely promising growth company that’s guaranteed to be successful, and you’d like to invest 10% of your capital in it. After your investment, the company would grow, and the stock price goes up tenfold.

If you had $10,000 of investable capital, you’d invested $1,000 and your position would be worth $10,000.

For comparison, if your starting capital would’ve been $100,000, you’d invested $10,000 and your position would be worth $100,000.

So, here’s the thing. The same percentages and returns are completely different in scale for wealthy investors.

When you’re just starting, even the best investments don’t feel like they’re getting you anywhere near that $1 million milestone.

Risk Aversion

Let’s take our previous example a bit further.

Both investors could’ve invested the same amount of $10,000 and gotten the same returns. So, why didn’t they?

Well, in real life, most people wouldn’t risk all their capital on one venture, no matter how promising it might be.

In other words, they are risk averse.

Interestingly enough, the risk isn’t the same for everyone. Comparing the two investors, the investor who has more capital can get greater returns with the same relative amount of risk.

So, once again, the beginner investor is the underdog.

Psychological Challenges

While getting wealthy by investing is often perceived as purely a numbers game, in reality, it’s largely a psychological endeavour.

Let’s take a look at a couple of the most common mental challenges.

Impatience. The truth is that wealth accumulates slowly. If there’s one thing that’s essential for an investor’s success, it’s patience.

Usually, when investors start to feel impatient, they take on too much risk and end up with undesirable results.

Achieving the one million milestone requires A LOT of patience.

Linear Thinking. Investing requires thinking on an exponential level. Unfortunately, we don’t do so well with exponential things.

It might have something to do with the fact that there’s not a lot of exponential growth in nature, so we haven’t really gotten accustomed to it.

When you’ve been investing for less than a decade and look at your return graphs, it does indeed seem linear.

The problem is that we start to expect exponential returns in a phase that can’t possibly yet have them.

We might think there’s something wrong with the process itself, while in reality, the process is sound, but it’s the thinking that’s flawed.

The Fear of Missing Out. A long-term investor can’t compare himself to short-term investors.

Let’s imagine your goal is to achieve the one million milestone with a regular, monthly investment plan.

The reality is that you can’t expect massive short-term returns, but you will eventually win in the long term. What’s difficult is to ignore the short-term winners.

If you feel like you’re missing out on returns, you start to modify your investment plan, and will most likely have bad long-term results.

The best medicine for fear of missing out is to stop comparing yourself to others, mind your own business, and trust the process!

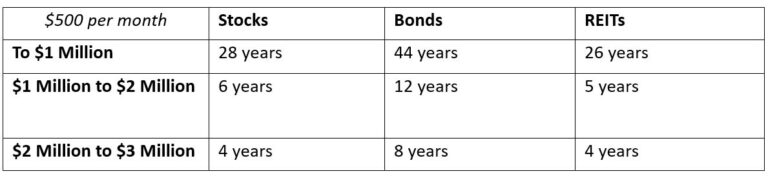

How Long Does It Take to Achieve A Million Dollars with Different Asset Classes

Usually, when we talk about achieving one million dollars with investing, we mean investing in stocks.

Then again, there are a lot of other asset classes out there, so it’s worthwhile to compare stock investing to the most common asset classes.

Let’s take a look at the average annualized returns of different asset classes:

Stocks. For the past 50 years, the S&P 500 has had an annualized return of 10.51% (dividends reinvested).

Bonds. The average bond return from intermediate government bonds for the past 100 years has been around 5.2%.

REITs. According to The Motley Fool, REITs have had an annualized return of 11.9% for the past 50 years.

It seems that the fastest way to reach your first million dollars would indeed be to invest in either stocks or REITs.

So, how long would it take, exactly?

Bear in mind that these are rough numbers at best, but they do give you an idea of what it takes to reach one million dollars in a reasonable time.

If you started investing $500 per month in either stocks or REITs, you’d have your first million in less than 30 years.

Bonds, on the other hand, would’ve taken over 40 years. While bonds may serve their purpose in retirement planning, for example, they’re not the optimal solution for making money.

All in all, there’s a reason why wealthy people save early.

Reinvest Your Dividends!

There’s a major difference in returns if you don’t reinvest your dividends.

As we discussed before, the S&P 500 had an annualized return of 10.51% with dividends reinvested.

If you didn’t reinvest your dividends, the returns would’ve only been 7.58%.

Now, let’s imagine you’d start to invest $500 per month in the S&P 500.

Here’s what would happen:

As you can see, if you didn’t reinvest your dividends, it would take you about 35 years to achieve your first million.

Then again, if you did reinvest your dividends, you’d already have more than $2 million by that time.

So, the easiest way to speed up the process is simply to reinvest, or if you’re a fund investor, invest in an accumulating fund instead of distributing one.

{kind=link}